NZ Super is critical to the majority of New Zealanders – with 40% of people aged 65 and over having virtually no other income besides NZ Super and another 20% having only a little more.

The importance of NZ Super is that it is part of stable and consistent retirement policy that allows people to plan over a long period of time and is a largely equitable system that is relatively simple to administer.

NZ Super is a pension for those aged 65. It is a cash payment that is not means-tested and has some residency-based eligibility criteria. The OECD refers to retirement income schemes as either tier 1, 2, or 3 schemes based on the objectives they aim to achieve. NZ Super is a ‘tier 1’ benefit as it aims to protect from poverty in old age. Tier 2 aims to ensure the adequacy of retirement income and tier 3 aims to raise the individual income replacement rate.

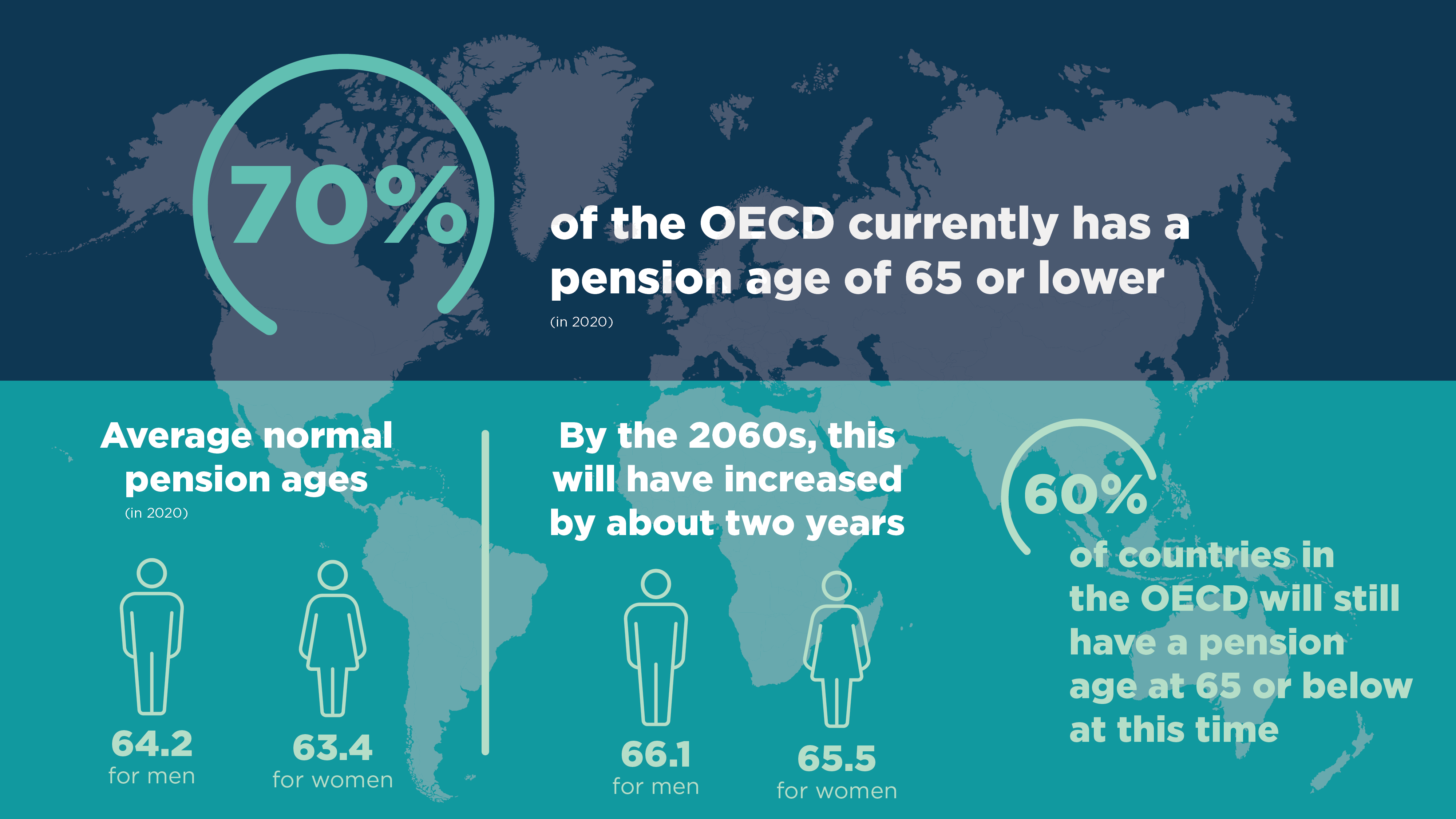

OECD pension age comparisons

In New Zealand to be eligible for NZ Super you need to be at least 65 years of age. Currently 70% of the OECD has a pension age of 65 or lower. While countries are increasing their pension age, the majority are only moving the age up to 65 over the next four decades. This means that by the 2060s 60% of OECD countries will still have pension ages of 65 or below.

More details about current and future pension ages in the OECD is available here.

New paper Summing up the Super Summit

The Super Summit took place on 21 March 2024 in Wellington hosted by Te Ara Ahunga Ora Retirement Commission. Focused on dissecting New Zealand’s superannuation system, it presented a comprehensive analysis of the fiscal challenges and opportunities inherent in pension policy.

Some of the country’s leading academics, political commentators, current and former politicians, journalists, and economists took part, sharing their views, insights, and recommendations to help shape the future of NZ Super.

An account of Super Summit has been developed, providing a summary of the views and insights shared by each of the panellists, including some of their recommendations or ideas to support future policy thinking.

New paper NZ Super Issues and Options

NZ Super is a taonga that protects New Zealanders from poverty in old age. However, NZ Super is said to be under fiscal pressure, due to forecast increase in expenditure in future years despite the simplicity of NZ Super’s design being internationally envied and New Zealand’s expenditure on its pension is relatively low compared to other OECD countries. This paper examines some policy options for NZ Super and the impacts of any change.

The paper restates the Retirement Commission’s position that the age of eligibility should stay at 65 for now, but good public policy requires a range of options to be assessed. There are other issues that matter as much as the age of eligibility. Political support for a stable long-term system is crucial.

Retirement income preferences in New Zealand study

Research shows widespread opposition to means-testing superannuation, and to raising the age of eligibility, but a willingness to increase taxes now rather than burden future generations.

We commissioned the University of Otago to conduct a study asking almost 1300 people throughout New Zealand about their preferences over seven aspects of retirement income policy. The same questions were asked in 2014 and the 2022 results are broadly similar to the results from 2014, with the three highest-ranked criteria still relate to means-testing, future taxes rates, and the age of eligibility.

Almost a quarter of people ranked keeping the age of eligibility at 65 as the most important aspect of NZ Super (compared to almost a fifth of people in 2014). The number of people who ranked the age of eligibility as the least important has fallen by 4%.

Raising the age of eligibility to 67 was ranked by 61% of respondents as the worst policy (of the seven options), making it the option ranked worst by the largest number of people. The unpopularity of this policy has increased relative to 2014.

NZ Super today

This paper covers how NZ Super operates including eligibility criteria, payments and how they are financed, and details the policy framework and settings.

New Zealand Super while travelling or moving overseas

Most people who receive NZ Super can still receive some NZ Super payments while overseas providing they have followed the rules before departing New Zealand. More details on receiving NZ Super in these circumstances can be found in our downloadable resource, and on the Work and Income website.

A snapshot of Aotearoa New Zealand’s superannuation history

Aotearoa New Zealand has had a pension system in place since the late 19th century aimed at preventing poverty amongst older people. Through the Social Security Act 1938 a two-tier public pension system was introduced that would last for nearly four decades. It featured a means-tested pension (Age Benefit) and a smaller universal superannuation payment.

Over the years, successive governments made various adjustments to the retirement pension schemes, including shifts in the ages of eligibility, increasing and then decreasing contributions, tax concessions, and changes to the percentages of wage ratios applied against pensions. Changes were made in the 1970s that created the New Zealand Superannuation [NZ Super] that we have today.

The beginning of the 21st century saw the establishment of the NZ Super Fund and KiwiSaver which have become the most significant innovations in retirement income initiatives in our recent history.

A more detailed account of the history of Aotearoa New Zealand’s retirement income, spanning 1898 to 2008, can be found in this earlier research paper commissioned by the Retirement Commission.

The following infographic outlines key moments in the history from 1898 to 2021

NZ Super in the 2022 RRIP

NZ Super was a key focus of the 2022 RRIP. Research was undertaken to better understand how reliant New Zealanders are on it and its importance as a pillar of retirement income Policies.

The key recommendation of the RRIP is that the age of eligibility to access NZ Super must remain the same. Any increase to the age of eligibility will only further disadvantage women, Māori, and Pacific People.

NZ Super research from previous RRIPs

A report prepared by MSD for the 2019 RRIP, provides an overview of public provision for retirement income in New Zealand. Download the report.

Another report commissioned for the 2019 RRIP considers the fiscal sustainability of current New Zealand superannuation settings. Download the report.

Other publications

The research listed below does not represent the views of TAAO. Different approaches, methods, and samples were used in these studies and this should be taken into account when interpreting the results.