A large-scale analysis of New Zealand’s Household Economic Survey (HES) has highlighted how the amount being spent on housing costs represents large proportions of people’s New Zealand Superannuation.

Te Ara Ahunga Ora Retirement Commission recently commissioned The Treasury to use the HES to analyse New Zealand’s housing costs across age groups as part of work delving into the adequacy of NZ Super for the growing numbers of people still paying off mortgages or paying rent past the ages of 65.

The findings will help inform the recommendations included in the final report of the 2022 Review of Retirement Income Policies Te Ara Ahunga Ora has been asked by Government to undertake.

The analysis shows those superannuitants still paying rent are much more likely to be spending 40% or more of their NZ Super income on housing, and long-term trends suggest more older householders are likely to be renters in the future.

Te Ara Ahunga Ora Director Policy, Dr Suzy Morrissey says the picture is worse for those still paying off mortgages, with 80% spending more than 40% of NZ Super on housing costs, and more than half spend more than 80% of NZ Super on housing costs.

“When comparing to those who own their homes outright this is almost totally reversed, with approximately 80% spending less than 40% of NZ Super on housing costs. More than 50% spend less than 20% of NZ Super on housing costs (55% of those aged 65-74 and 70% of those aged 75+),” she says.

“It is important to note that this analysis of housing costs is relative to the income received from NZ Super only and does not factor in other income. However, NZ Super is currently the only income for 40% of those 65 and over, and 20% only have a little more.”

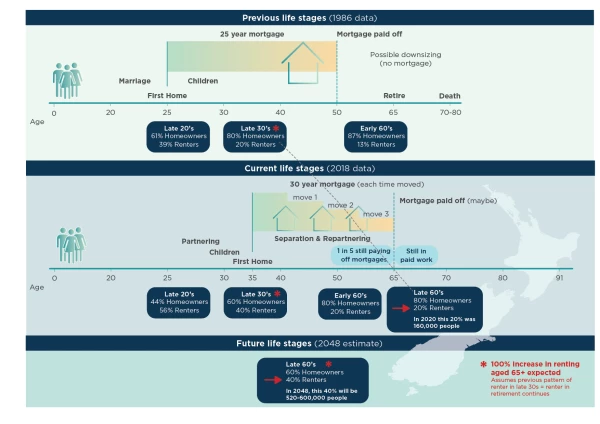

A snapshot of how housing has changed over the last three decades or so, shows:

- In 1986, 87% of those in their 60s were homeowners, with mortgages paid off, and for the most part were not in paid work.

- In 2018, 80% of those in their early 60s were homeowners, but 1 in 5 were still paying off mortgages, 20% paying rent, and many still in paid work. Mortgage and rent costs have been rising faster than outright ownership costs.

- Based on current trends, there is going to be a 100% increase in people renting aged 65 and over.

- Long term the balance of homeownership is expected to shift to 60% homeowners and 40% paying rent. By 2048, this 40% will equate to up to 600,000 people.

“What all of these insights highlight is the impacts of not owning your home outright or paying rent when you are very reliant, or completely reliant on NZ Super to cover those costs,” says Dr Suzy Morrissey.

“It’s a real challenge for people to make ends meet if they are having to use substantial amounts of their NZ Super to cover housing costs.

“When NZ Super was introduced, it was with the underlying assumption that those accessing it would be mortgage-free homeowners.

“Today, the reality is very different. There are declining home ownership rates, more people needing to continue working longer because they still have mortgages to pay, are paying rent, or haven’t been able to save enough to retire.”

HOUSING GRAPHIC: Housing stages through the ages – 1980s, 2018 and in the future

Notes to editors:

About the RRIP

Under the New Zealand Superannuation and Retirement Income Act 2001, the Retirement Commissioner is required to carry out a Review of Retirement Income Policies (RRIP) every three years and report to Government. Key topics to be focused on for the 2022 review relate to three broad areas comprising New Zealand Superannuation, housing, and private savings including KiwiSaver.

More information, including the terms of reference, is available here.

About NZ Super

New Zealand Superannuation (NZ Super) is the government pension paid to Kiwis aged 65 and older.

Any eligible New Zealander receives NZ Super, regardless of:

- How much they earn through paid work

- Their savings and investments

- Any other assets they own

- What taxes they have paid.

- 40% of all over 65s have less than $100 pw from other sources (40% of singles have no other income).

- the next 20% have on average around 70% of their income from NZS and other government transfers

Media contacts:

For more information, or to arrange any interviews contact:

Anika Forsman | Director, Stakeholder Relations

Mobile +64 21 246 4302