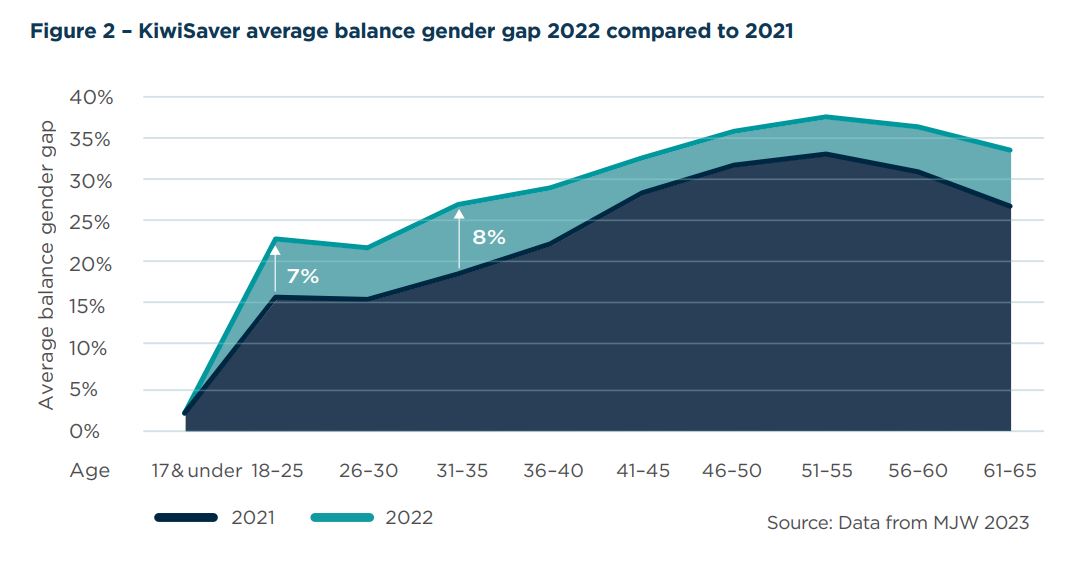

New data from Te Ara Ahunga Ora Retirement Commission has highlighted that there is a 25% gender gap on average KiwiSaver balances, up 5% in one year from the 20% gap identified in 2021.

The research found gender gaps in every age group category widened, with larger gaps opening in younger ages groups, up 7% for 18 – 25 year olds (now 23%) and up 8% for 31 – 35 year olds (now a total 27% gap).

KiwiSaver average balance gender gap 2022 compared to 2021

Te Ara Ahunga Ora engaged Melville Jessup Weaver (MJW) actuaries to collect demographic data on KiwiSaver as at 31 December 2022 to provide an update to the data first collected as at 31 December 2021.

The data was gathered from over three million KiwiSaver members and represents approximately 94% of the total KiwiSaver member base. All providers from the previous 2021 report participated again, as well as new providers.

Te Ara Ahunga Ora Director, Policy and Research, Dr Suzy Morrissey says the MJW report highlights the importance of closing gender pay gaps and the implications for KiwiSaver balances and retirement.

“The data shows that within the period of one year the difference between KiwiSaver balances for men and women has increased, highlighting the continued gender savings gap.”

“This research builds a picture of the challenges women face to grow their KiwiSaver balances. Analysis of the widening gap does not appear to be explained by fund choice, withdrawal, or suspension behaviour of women compared to men.”

“The widening of the gap at younger ages is particularly concerning because of compounding interest. Money invested earlier will have time to grow, but if women's balances are lower than men's in younger life, they will likely remain lower,” says Dr Morrisey.

Additional analysis was carried out to understand the impact of significant hardship withdrawals, first home purchase withdrawals, and savings suspensions using additional data from IRD. Withdrawals and suspensions did not explain the differences - more men were on suspensions and had withdrawn more money. It was noted that data does not capture those who have left paid work and no longer contribute (this is not a savings suspension).

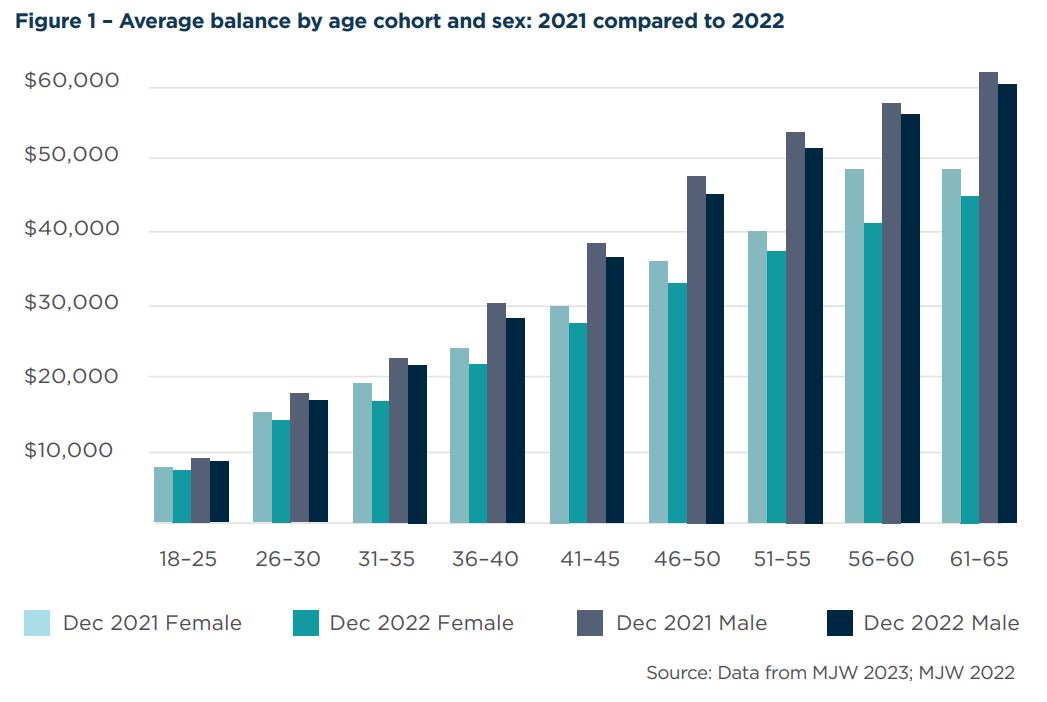

The average KiwiSaver balance as at 31 December 2022 was $27,379, a drop of 5.7% from 2021. This reflects poor financial market conditions over the 2022 year. Balances dropped across all ages, and both genders were impacted.

- For males, the average balance fell 3.2% (to $31,496).

- For females, the average balance fell 7.1% (to $25,144).

The research has also investigated member balances across age and gender by fund type for the first time. It found that more than one third of all funds under management are assets invested in growth funds, this allocation decreases with age.

Men have more assets invested in growth funds, while women have more assets invested in conservative funds. This difference is smaller at younger ages and more pronounced for those nearing age 65, and over 65.

Analysis suggests that women are not necessarily more risk averse, as both men and women tend to be invested in lower risk funds if they have small balances and have more growth assets if they have larger balances. Women's lower balances (on average) may lead them to be less risk-seeking.

The widest gaps of average balances are still between men and women in their 40s and 50s, which likely reflects the combined impact of the gender pay gap, time out of paid work, and the higher percentage of women than men that work part-time.

Average balance by age cohort and sex: 2021 compared to 2022

- On average, women in their 40s have approximately $10,000 (or 34%) less KiwiSaver than men

- On average, women in their 50s have approximately $14,500 (or 37%) less KiwiSaver than men

“Lower KiwiSaver balances have a significant impact on retirement for women, who on average live longer than men and need to fund their retirement for longer,” says Dr Morrissey.

The 2022 Review of Retirement Income Policy found that 40% of people aged 65 and over have virtually no other income besides NZ Super and another 20% only have that, and a little more.

Notes to editors:

About Melville Jessup Weaver (MJW) KiwiSaver Demographic Report

Method

MJW approached several KiwiSaver providers asking for aggregated data covering the membership of their schemes. Providers were asked to fill in a simple spreadsheet giving the number of members for different age and gender combinations, and the average savings balance. Data was provided in 2023 giving a snapshot as at 31 December 2022.

Providers covering 3,058,230 members with total balances of $83.73 billion responded. According to the IRD, in December 2022 there were 3,249,512 KiwiSaver members in total, meaning that this survey covered approximately 94% of the total KiwiSaver member base.

For the additional data collected for the KiwiSaver fund type analysis, the largest KiwiSaver schemes were asked to submit more detailed data. There is significantly more complexity in this project, therefore for timeliness and accuracy reasons, a smaller sample was accepted.

Providers covering 2,147,944 members with total balances of $54.14 billion responded. According to the IRD, in December 2022 there were 3,249,512 KiwiSaver members in total, meaning that this KiwiSaver fund type survey covered approximately two thirds of the total KiwiSaver member base.

While a large sample, it is possible that the results reflect some biases and due caution should be applied to interpreting the results. Also, it should be noted that some gender information was unavailable. In this report, total figures include data relating to members where gender is unknown. However, the analysis of males and females excludes data relating to members where gender is unknown. KiwiSaver providers do not collect information on ethnicities, only by age and gender.

ENDS

For interviews contact:

Elizabeth O’Halloran | Communications Lead

021 749 467